This real estate investment glossary brings together 20 key terms that every investor should know before analysing a real estate opportunity. The world of professional real estate investment has its own language. When analysing an opportunity, reviewing an investment dossier or speaking with a manager, it is common to come across terms such as IRR, NPV, MOIC, yield, LTV, capex, value add, GDV or real estate due diligence.

Understanding this vocabulary does not automatically make someone an expert, but it does make it easier to read an opportunity with greater clarity. For example, IRR helps compare projects with different timelines, LTV helps assess the level of debt, capex reflects the investment required to improve the asset, and real estate due diligence helps identify risks before committing capital.

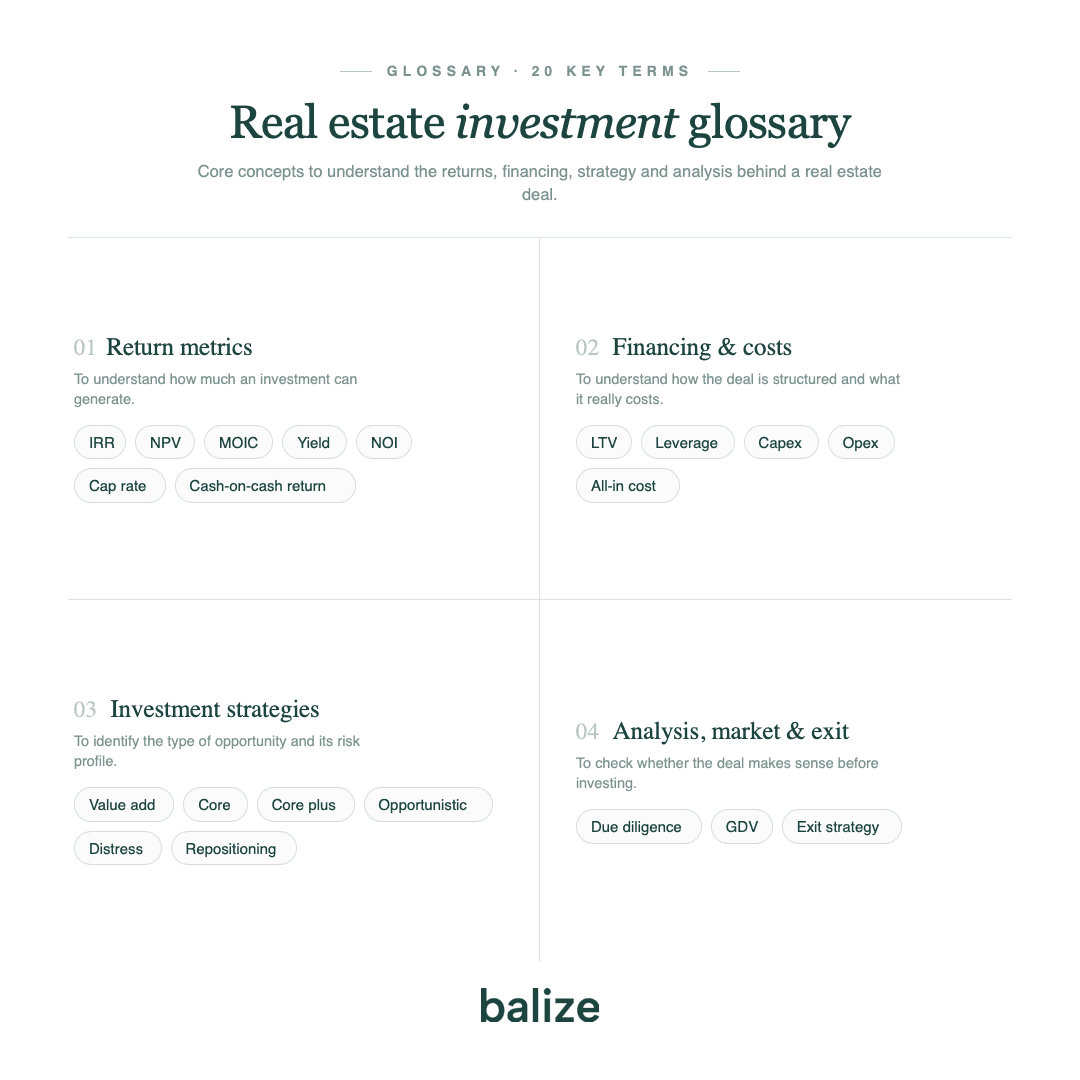

To make it easier to consult, this real estate investment glossary is structured into four blocks:

1. Return metrics.

2. Financing and costs.

4. Concepts related to analysis, market and exit.

Throughout the article, we will use the same fictional example* to explain the concepts: an older residential property in an established area, acquired for **€800,000**, requiring a full renovation and other associated costs, bringing the estimated total cost to **€1,050,000**, with an expected sale price after renovation of **€1,300,000**.

*This example is for illustrative purposes only and does not represent a real transaction.

Return metrics

1. IRR — Internal Rate of Return

IRR is the estimated annualised return of an investment, taking into account all cash flows and the timing in which they occur.

Why is it important?

It is one of the most widely used real estate investment metrics for comparing projects with different timelines. Achieving a return in 10 months is not the same as achieving it in 24 months. IRR makes it possible to standardise the analysis and compare investments with different durations.

Ejemplo o uso prácticoExample or practical use

In the example of the residential property, the investor acquires the asset, carries out the renovation and sells the renovated property. If the transaction is completed in 12 months, the IRR will be higher than if the same profit is achieved in 18 or 24 months. That is why, in value-add projects, the execution and sale timeline is just as important as the final profit. A transaction may appear profitable in absolute terms, but lose appeal if it takes too long to complete.

2. NPV — Net Present Value

NPV calculates the present value of the future cash flows of an investment, discounted at a given rate and subtracting the initial investment.

Why is it important?

It helps determine whether an investment creates value compared with a reference alternative. A positive NPV indicates that the project generates value above the minimum return required by the investor. A negative NPV may indicate that the transaction does not compensate for the risk assumed.

Example or practical use

Suppose the investor requires a minimum return to enter into the residential property transaction. NPV would make it possible to assess whether, after considering the acquisition, renovation, expenses, financing and final sale, the project generates sufficient value compared with that minimum required return. If the NPV is positive, the transaction may make financial sense. If it is negative, the investor may need to renegotiate the purchase price, review costs or discard the transaction.

3. MOIC — Multiple on Invested Capital

MOIC measures how many times the invested capital is recovered. It is calculated by dividing the total capital recovered by the capital invested.

Why is it important?

It complements IRR because it shows the absolute return on the investment. IRR measures annualised return, while MOIC shows how much the capital is multiplied. Both metrics should be analysed together.

Example or practical use

If, in the residential property transaction, the investor contributes €500,000 of equity and recovers €625,000 at closing, the MOIC would be 1.25x. This means that for every euro invested, the investor recovers €1.25, including the return of the initial capital and the profit generated. However, MOIC says nothing about time on its own. A MOIC of 1.25x over 12 months does not have the same interpretation as a MOIC of 1.25x over 36 months.

4. Gross yield and net yield

Gross yield measures the annual rental income generated by an asset in relation to its purchase price. Net yield adjusts that return by deducting operating expenses, taxes, maintenance and other associated costs.

Why is it important?

Gross yield can provide an overly optimistic view. Net yield is more useful for understanding the real return of a rental asset.

Example or practical use

If, instead of selling the renovated property, the investor decides to rent it for €4,000 per month, the gross annual rent would be €48,000. Based on a total cost of €1,050,000, the gross yield would be approximately 4.6%. However, if there are annual expenses such as community fees, property tax, insurance, maintenance or management costs amounting to €8,000, the net rent would be €40,000 and the net yield would be lower. That is why, for rental assets, net yield provides a more realistic view.

5. Cash-on-cash return

Cash-on-cash return measures the annual net cash flow received by the investor in relation to the equity invested.

Why is it important?

It is particularly useful when financing is involved, because it measures the return on the actual equity contributed, rather than on the total value of the asset.

Example or practical use

Imagine the investor contributes €500,000 of equity and finances the rest with debt. If they decide to rent the renovated property and, after operating expenses and debt payments, receive €30,000 net per year, the cash-on-cash return would be 6%. This metric helps understand what return is generated by the capital actually contributed by the investor, especially in leveraged transactions.

6. NOI — Net Operating Income

NOI is the net operating income of a real estate asset. It is calculated by subtracting operating expenses from the income generated by the property, before debt, depreciation and taxes.

Why is it important?

It is a key metric for valuing income-generating assets, especially offices, retail units, residential rental buildings or logistics assets. It shows the asset’s real ability to generate operating income.

Example or practical use

If the renovated property is rented for €48,000 per year and operating expenses amount to €8,000, the NOI would be €40,000. This figure allows the asset to be analysed before taking financing into account. In this way, the property can be valued based on its income-generating capacity, regardless of how the transaction has been financed.

7. Cap rate — Capitalisation rate

The cap rate relates the annual NOI of an asset to its market value or acquisition price. It is used to estimate the return of a property based on its income.

Why is it important?

It allows income-generating assets to be compared and helps assess whether a property is expensive or attractive in relation to the income it produces. It is also used to estimate the value of an asset based on its NOI.

Example or practical use

If the renovated property generates an NOI of €40,000 and is valued at €1,300,000, the cap rate would be approximately 3.1%. This figure can be compared with similar assets in the area. If equivalent properties offer higher cap rates, the investor should assess whether the expected sale price is too high or whether the asset has distinctive features that justify that valuation. To explore these metrics in more detail, you can read our guide onhow to calculate the profitability of a real estate investment.

Financing and costs

8. Leverage

Leverage consists of using debt to finance part of a real estate investment.

Why is it important?

It can increase the return on equity if the transaction performs well, but it also increases risk if income falls, costs rise or the sale is delayed.

Example or practical use

In the residential property transaction, the investor may choose not to finance the entire purchase with equity and instead use bank financing to cover part of the purchase price. This allows the investor to allocate less initial equity to the project. However, leverage involves financial payments, maturities and obligations. If the renovation is delayed or the sale takes longer than expected, financing costs can reduce the final return.

9. LTV — Loan to Value

LTV is an indicator that measures the percentage of debt in relation to the total value of the asset. It shows which part of the transaction is financed by the investor and which part is financed through debt, usually a bank loan.

Why is it important?

The higher the LTV, the higher the level of leverage and, generally, the higher the financial risk. It can also affect the return on the equity invested.

Example or practical use

If the property is acquired for €800,000 and the bank finances €480,000, the initial LTV would be 60%. This means that 60% of the purchase price is covered by debt and the remaining 40% by equity. If the transaction is executed correctly, debt can improve the return on the capital invested. However, if the sale is delayed or the final price falls, the level of debt can also increase financial pressure.

10. Capex — Capital Expenditure

Capex is the investment allocated to improving, renovating, refurbishing or transforming a real estate asset.

Why is it important?

It is a key item in value-add projects, repositioning strategies or full renovation projects. Poorly estimated capex can significantly reduce the profitability of a transaction.

Example or practical use

In the example property, capex would include the full renovation: demolition, installations, bathrooms, kitchen, carpentry, air conditioning, flooring, painting, lighting and potential energy efficiency improvements. If capex is initially estimated at €130,000, but structural issues or obsolete installations arise during the works, the cost may increase. For this reason, capex must be analysed carefully before acquiring the asset.

11. Opex — Operating Expenditure

Opex refers to the operating expenses required to maintain and manage a real estate asset.

Why is it important?

It directly affects the net return of the property. In rental assets, high opex can reduce NOI and, therefore, the value of the asset.

Example or practical use

If the investor decides to hold the renovated property for rental, they will have to assume recurring costs such as community fees, insurance, maintenance, repairs, administration or rental management. All these expenses form part of opex. Even if the gross rent appears attractive, high opex can significantly reduce the net profitability of the asset.

12. Coste all-in

All-in cost is the total cost of a real estate transaction, including acquisition, taxes, legal expenses, renovation, financing, fees, commercialisation and other associated costs.

Why is it important?

It allows the transaction to be analysed realistically. Looking only at the purchase price is not enough: it is necessary to understand how much it actually costs to take the project through to sale, rental or stabilisation.

Example or practical use

In the example, the property is acquired for €800,000, but that is not the real cost of the transaction. If taxes, notary fees, registration costs, renovation, technical fees, licences, financing, decoration and commercialisation are added, the estimated total cost reaches €1,050,000. This is the figure that should be compared with the expected sale price of €1,300,000. Analysing only the purchase price would provide an incomplete view.

Real estate investment strategies

13. Value add

Value add is a real estate investment strategy that seeks to create value through renovation, repositioning, rental uplift, change of use or active management of the asset.

Why is it important?

Unlike a passive investment, the outcome depends largely on the ability to identify the asset’s potential and correctly execute the improvement plan.

Example or practical use

The example property is a value-add transaction because the investor is not acquiring an already optimised asset. They are acquiring an older property, with an inefficient layout and renovation needs, in order to transform it into a more attractive product for the market.

Value creation does not depend solely on market appreciation, but on improving the asset, adapting the product to the target buyer and selling it under better conditions.

You can explore this concept further in our article on value-add real estate investments.

14. Core / Core plus

Core refers to stabilised real estate assets, well located and with a lower risk profile. Core plus includes slightly more risk or improvement potential, while still maintaining a relatively conservative profile.

Why is it important?

It helps classify the risk and return profile of an investment. Not all real estate strategies have the same risk level or investment horizon.

Example or practical use

The older property in the example would not be considered core, because it requires renovation, execution and a subsequent sale. A core asset could be, for example, a prime residential property that is already renovated, leased long term and generating stable income. It could be considered core plus if it were well located, generating income, but still had some room to improve rents, efficiency or positioning without requiring a complex renovation.

15. Opportunistic

Opportunistic is an investment strategy with higher risk and higher potential return. It often involves complex assets, special situations, development, distressed debt or intensive repositioning.

Why is it important?

It helps identify transactions with greater upside potential, but also with greater uncertainty. These opportunities require experience, deep analysis and execution capability.

Example or practical use

If the property in the example had relevant urban planning issues, a pending legal situation, irregular occupation or a much more complex transformation, the transaction could be closer to an opportunistic strategy. The return potential could be higher if those issues are resolved, but the risk would also be higher. Not every discounted opportunity compensates for the complexity involved.

16. Distress

Distress refers to assets or situations in which the seller needs to divest due to financial, legal, operational or personal pressure.

Why is it important?

It can generate opportunities to acquire assets at a discount, but it usually involves greater complexity and risk. It is essential to understand the cause of the distress.

Example or practical use

If the owner of the property needs to sell urgently due to liquidity issues, debt or financial pressure, the asset may come to market below its potential value. This situation could generate an opportunity for the investor. However, before acquiring the asset, it is important to understand why it is being sold at a discount: it may be a specific need of the seller, or there may be technical, legal or commercial issues that justify the price.

17. Real estate repositioning

Real estate repositioning consists of transforming an asset so that it occupies a more competitive or more valuable position in the market.

Why is it important?

It is a common way to create value in value-add strategies. It may involve renovation, change of use, improved specifications, space redistribution or a change in target audience.

Example or practical use

In the case of the property, repositioning does not simply mean renovating the bathrooms and kitchen. It means turning an older, less competitive property into an updated, functional home aligned with demand in the area. This may include a new layout, higher-quality specifications, energy efficiency improvements and a more attractive commercial presentation. The objective is for the asset to stop competing as an outdated property and start competing as a higher-value renovated product.

Analysis, market and exit

18. Real estate due diligence

Real estate due diligence is the process of carrying out a thorough review of an asset before acquisition. It analyses legal, technical, urban planning, tax and financial aspects.

Why is it important?

It helps identify risks before committing capital. An urban planning limitation, a registry charge or a technical issue can affect the viability of the transaction.

Example or practical use

Before acquiring the property, the investor should review ownership, charges, registry status, technical condition, required licences, homeowners’ association matters, potential community charges, urban planning regulations and the renovation budget. If this review reveals a limitation that prevents the planned renovation from being executed, the project may no longer make sense. Due diligence helps detect these risks before capital is committed.

19. GDV — Gross Development Value

GDV is the estimated gross value of the asset once the project, renovation or transformation has been completed.

Why is it important?

It is a key variable in value-add or development projects, because it allows the expected final value to be estimated and compared with the total cost of the transaction.

Example or practical use

In the reference transaction, if the renovated property is expected to sell for €1,300,000, that amount would be the projected GDV. The investor should compare this value with the all-in cost of €1,050,000 to assess whether there is sufficient margin. If the GDV decreases due to market changes or an overly optimistic valuation, the expected profit can be significantly reduced.

20. Exit strategy

The exit strategy defines how the investment will be monetised: sale, rental, refinancing or holding the asset in the portfolio.

Why is it important?

A real estate investment should always be analysed with the potential closing of the transaction in mind. The expected return depends not only on buying well, but also on selling, renting or refinancing under reasonable conditions.

Example or practical use

In the example, the main strategy could be to sell the renovated property to an end buyer. However, it is advisable to consider alternatives. If the sales market slows down, the investor could assess temporarily renting the asset or adjusting the commercial strategy. Defining the exit before buying helps avoid improvised decisions and makes it easier to assess liquidity, price and timing risks. If you want to see how these concepts are applied in practice, you can read our article onreal estate investment opportunities.

Conclusion

This real estate investment glossary can serve as a starting point for better interpreting an investment dossier, comparing opportunities and understanding the main risks of a transaction. Metrics such as IRR, NPV, MOIC, yield or cap rate help assess profitability; concepts such as LTV, capex, opex or all-in cost help understand the financial structure; and terms such as value add, real estate due diligence, GDV or exit strategy help evaluate the viability of a project.

In real estate investment, understanding the vocabulary is not just a theoretical exercise. It is a practical tool for reading a project more clearly, comparing opportunities and making more informed decisions.

At Balize, we apply these concepts when analysing real estate opportunities, assessing each project from the perspective of profitability, risk, execution and exit. If you would like to access our private investor club, you can request registration on our platform: https://app.balize.com/auth/register.