Analysing a value-add real estate project requires first understanding what makes this type of transaction different. In a value-add real estate investment, the objective is not to acquire an already stabilised asset, but to identify a property with improvement potential and create value through renovation, real estate repositioning, use optimisation or active management.

This type of strategy can be attractive because it allows value to be created beyond the natural evolution of the market. However, it also requires a more rigorous analysis: it is not enough to identify an asset with potential; it is necessary to determine whether the transformation is viable, whether there is demand for the final product, whether the costs are properly estimated and whether the planned exit strategy is realistic.

In this article, we focus on the practical side: how to analyse a value-add real estate project before investing, reviewing the market, the asset, the financial model, execution, risks and exit strategy. However, if you would like to explore the value-add concept in more detail, you can read our article on value-add real estate investments. In it, we explain what they are, what benefits they can offer, how to identify these types of opportunities and which factors influence their profitability.

The analysis methodology: from opportunity to investment decision

When an asset with potential is identified, the analysis must turn that initial opportunity into a well-substantiated investment decision. To do so, it is important to follow a clear sequence:

1. Market validation

2. Asset review

3. Definition of the final product

4. Development of the financial model

5. Execution assessment

6. Creation and validation of the exit strategy

This order is important because it prevents the transaction from being analysed backwards. If the market cannot absorb the final product, the financial model loses strength. If the asset presents technical, legal or urban planning limitations, the budget may become misaligned. And if the exit is not clearly defined, the expected return may depend on assumptions that are difficult to support.

The purpose of the methodology is not to confirm that the asset appears attractive, but to determine whether the transaction is sufficiently supported by data, scenarios and realistic execution.

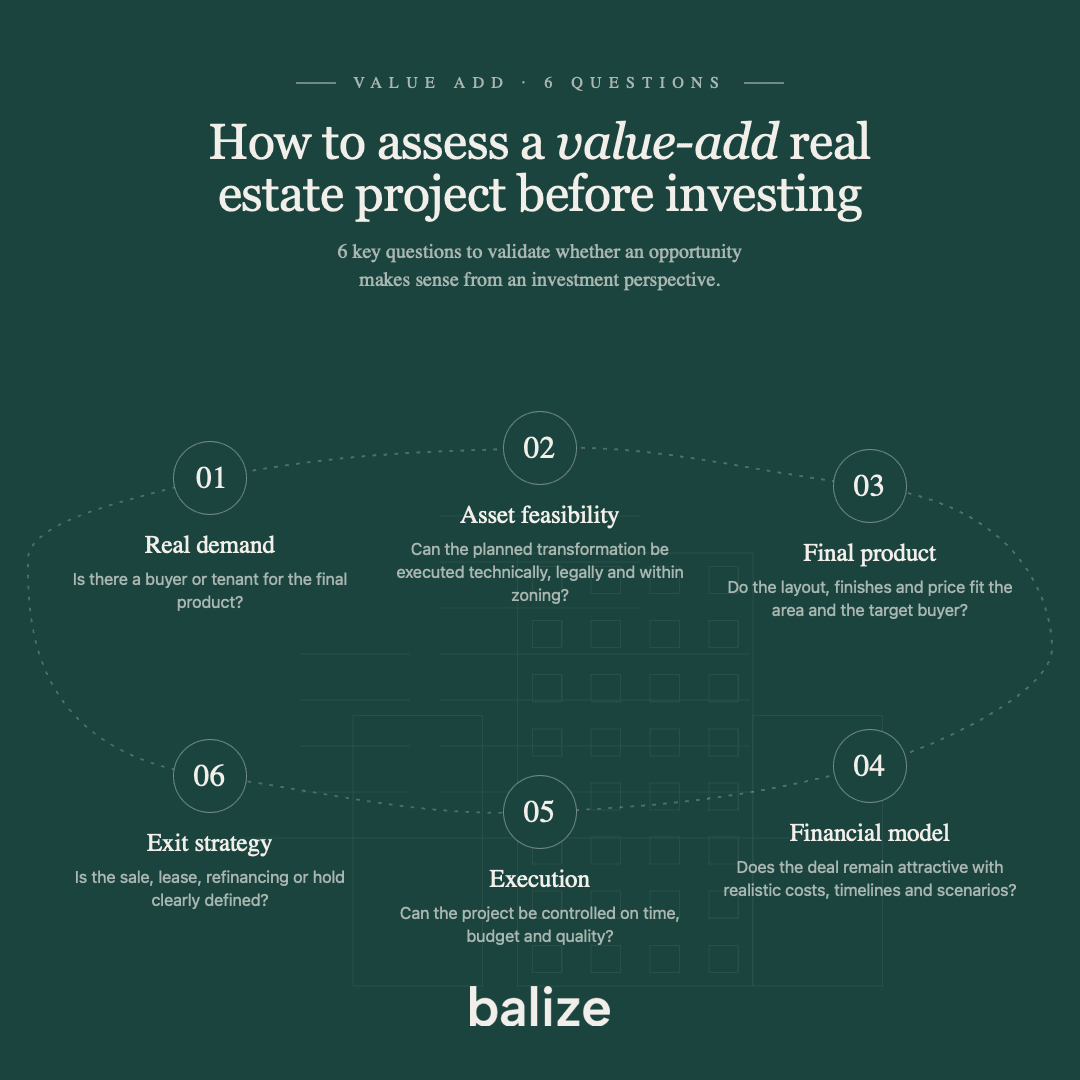

The six key questions when analysing a value-add real estate project

1. Is there real demand for the final product?

It is not enough for the current property to appear inexpensive or to be located in a good area. When you identify an asset that requires transformation or adaptation to maximise its value, it is important to assess, before launching the transaction, whether the renovated product will attract buyers or tenants willing to pay the target price.

2. Does the asset allow the planned transformation to be carried out?

Once demand for the final product has been validated, the next step is to determine whether the planned transformation is actually viable. This requires analysing the technical condition of the asset, any potential legal limitations, applicable urban planning regulations, required licences and any factor that could affect the renovation, the intended use or the execution timeline.

3. Does the final product fit the area and the target buyer?

A renovation may be well executed, but still fail to create value if the layout, specifications, price or commercial positioning do not respond to real market demand. For this reason, before defining the project, it is important to identify who the final buyer or tenant will be and what they expect to find in that location.

The objective is not to renovate for the sake of renovating, but to create a competitive product compared with similar assets in the area and aligned with the planned exit strategy.

4. Can the financial model remain attractive with realistic costs and timelines?

The financial model should not be built only around the most likely scenario, but also around less favourable scenarios. It is therefore important to assess what happens if costs increase, if the sale takes longer than expected or if the final price comes in below initial expectations.

In a value-add project, small deviations in construction costs, timelines or exit price can have a significant impact on profitability. For this reason, the analysis must determine whether the transaction still makes sense under prudent assumptions and whether there is sufficient margin to absorb unexpected events without compromising the expected outcome.

5. Can the value-add investment project be controlled in terms of time, budget and quality?

Execution is one of the most critical aspects of a value-add transaction. It is not enough for the initial analysis to look attractive: the project must be capable of being delivered within a reasonable timeline, with a controlled budget and with quality standards aligned with the final product.

This requires coordinating the technical team, licences, construction works, suppliers, commercialisation and transaction closing. Any material deviation in timelines, costs or quality can directly affect the expected return and the exit plan.

6. Is there a clear and viable exit strategy?

inally, before acquiring the asset, it is essential to define how the exit from the transaction will be materialised. The project may be structured around the sale of the renovated property, its rental, a potential refinancing or holding the asset in the portfolio. Each alternative has different implications in terms of timeline, liquidity, expected return and risk level. For this reason, the exit strategy must be aligned from the outset with the final product, market demand and the investment objectives.

If any of these questions required to analyse a value-add investment project does not have a solid answer, the transaction should be reviewed before committing capital.

How to analyse a value-add real estate project step by step

Once the key questions have been answered, the next step is to develop the analysis in an orderly way. To assess whether a value-add real estate project makes sense from an investment perspective, each area should be reviewed separately: market, asset, final product, financial model, execution and exit.

Step 1: validate the location and demand for the final product

The first step is to analyse the market. The asset should not be assessed only in its current condition, but also in relation to the final product that will be created after the transformation. To do so, it is important to review indicators such as the average price per square metre, available supply, absorption rate, average sales period, price trends, target demand and renovated comparable assets in the area.

It is also important to understand who may buy or rent the final product: families, professionals, international buyers, investors, end users or profiles looking for a renovated property in an established area.

Location is an essential factor, but it does not automatically turn every asset into a good investment. An attractive area must be accompanied by a well-designed product, a reasonable entry price and an exit strategy aligned with real market demand.

Step 2: carry out a complete real estate due diligence

Once the market has been validated, the next step is to carry out a real estate due diligence. This review should cover four areas:

- Legal: ownership, charges, contracts, leases or potential limitations are reviewed.

- Technical: the condition of the property, structure, installations, energy efficiency, renovation needs and potential hidden risks are analysed.

- Urban planning: the intended use is checked to confirm whether it is viable and whether the necessary licences can be obtained.

- Financial: expenses, taxes, maintenance costs, potential community charges and any item that may affect the total budget are reviewed.

This step is particularly relevant in real estate repositioning transactions, as an issue not detected at the outset may later become a delay, cost overrun or loss of profitability.

Step 3: define the final product

In a value-add transaction, renovation alone is not enough. It is necessary to define what product will be delivered to the market and why that product makes sense in that specific location.

This involves reviewing the layout, usable areas, number of bedrooms, functionality, specifications, energy efficiency, interior design and commercial positioning. Floor plans, renders and layout proposals are not merely decorative elements: they help validate whether the transformed asset truly responds to what the target buyer or tenant is looking for.

A good project does not only improve the physical condition of the property. It also improves its appeal, liquidity and ability to compete against similar assets.

Step 4: build the real estate financial model

The real estate financial model must answer a simple question: does the transaction remain attractive after incorporating all costs, timelines and potential deviations?

The model should include the total cost of the transaction: acquisition, taxes, renovation, financing, technical fees, licences, commercialisation, operating expenses and other associated costs. It should also estimate the final value of the transformed asset, known as GDV or Gross Development Value.

From there, metrics such as margin, IRR and MOIC are analysed. No metric should be interpreted in isolation. An expected return may appear attractive, but it can lose strength if it depends on overly optimistic assumptions or an unrealistic exit. To explore these metrics further, you can read our guide on the profitability of a real estate investment.

In addition to the base case, it is advisable to work with alternative scenarios. A solid analysis should test what happens if the sale takes longer, if the final price is lower than expected or if renovation costs increase.

Step 5: assess execution and timeline

In a value-add project, execution is where much of the projected value is either confirmed or lost. For this reason, before investing, it must be clear who will execute the project, with what budget, within what timeframe and under what level of control.

The operating plan should translate into a realistic timeline, with phases such as acquisition, licences, renovation, commercialisation, sale and closing. In this type of transaction, time is not only an organisational issue: it is a financial variable. Any delay can affect the expected return.

It is also important to review the technical team, contractors, construction milestones, cost control and the responsibilities of each party. A good opportunity can deteriorate if the renovation is delayed, if material deviations arise or if commercialisation is not prepared from the outset.

Step 6: define the exit before buying

One of the main criteria for evaluating a real estate project is having a clear exit before acquiring the asset. The transaction may end in a sale, rental, refinancing or holding the asset in the portfolio, but each option has different implications in terms of timeline, liquidity and profitability.

Defining the exit helps avoid improvised decisions. It also makes it possible to assess whether the entry price, transformation cost and expected final value leave sufficient margin to compensate for the risk assumed.

The exit must be aligned with the final product and real market demand. Without a clear exit strategy, even a well-executed renovation can become difficult to monetise.

Common mistakes when analysing a value-add project

When analysing a value-add project, mistakes usually arise when one stage of the analysis is approached superficially or based on overly optimistic assumptions.

In the market analysis, one of the most common mistakes is using comparables that are not truly equivalent: assets in better condition, with higher specifications, in more liquid locations or with exit prices that are not representative. This can lead to overestimating the final value of the project.

In terms of real estate due diligence, the main risk is failing to detect legal, technical or urban planning limitations in time. A registry charge, obsolete installation, more complex licence than expected or use restriction can alter the budget, timeline or even the viability of the transaction.

Regarding the final product, the most frequent mistake is designing a renovation that does not respond to real market demand. A property may be well finished, but still fail to create value if the layout, specifications, price or commercial positioning do not fit the target buyer or tenant.

In the financial model, the most common error is underestimating costs or working with overly favourable scenarios. If the analysis depends on selling at the highest price in the market, completing the works without deviations or meeting a very tight timeline, the safety margin may be insufficient.

In the execution phase, one of the most relevant mistakes is failing to anticipate delays, changes in scope or lack of coordination between technical teams, contractors, licences and commercialisation. In a value-add transaction, a deviation in time or budget can directly affect the expected return.

Finally, in the exit strategy, the most important mistake is not defining from the outset how the transformed asset will be monetised. Without a clear exit — sale, rental, refinancing or holding the asset in the portfolio — the transaction may be exposed to improvised decisions or lower liquidity than expected.

A good analysis does not seek to confirm that a transaction looks attractive, but to determine whether it still makes sense when risks, costs, timelines and less favourable scenarios are incorporated.

How Balize applies this methodology

Balize was created with the objective of democratising access to real estate investment opportunities that have traditionally been reserved for profiles with greater operational capacity, technical knowledge or direct access to the market.

We carry out comprehensive management of each transaction: opportunity sourcing, location and market analysis, legal, tax, technical and urban planning due diligence, transaction structuring, renovation follow-up, cost control and coordination of commercialisation.

This model allows investors to access selected real estate projects without having to directly assume the entire process of sourcing, analysis, acquisition, renovation, management and sale of the asset. The transaction is supported by an expert team and an analysis methodology designed to assess each opportunity from the perspective of profitability, risk, execution and exit.

In value-add projects, this management is particularly relevant because, as mentioned above, value creation does not depend only on acquiring an asset with potential, but on correctly executing the planned transformation and controlling the variables that may affect the final outcome.

Conclusion

Analysing a value-add real estate project involves much more than assessing the purchase price or the apparent renovation potential. It requires understanding the location, validating demand, reviewing the asset, defining the final product, building a realistic financial model, structuring execution and clearly defining the exit strategy before investing.

In this type of transaction, profitability does not depend solely on the market, but also on the quality of the analysis and the ability to execute each phase of the project correctly. For this reason, a solid methodology not only helps identify opportunities with potential, but also allows investors to discard those that do not adequately compensate for the risks, costs or timelines involved.

Ultimately, in a value-add strategy, value creation begins long before the renovation itself. It starts with the preliminary analysis, the rigorous selection of the asset and the ability to turn an opportunity into a project that is viable, measurable and executable.

Analysing a real estate project with a clear methodology helps support more informed decision-making, but it does not eliminate the inherent risks of an investment. Results may vary depending on timelines, costs, market evolution, asset liquidity and project execution. This article is for informational purposes only and does not constitute financial, tax, legal or investment advice. Each transaction should be assessed based on its specific documentation and the profile of each investor.