The return on a real estate investment can be assessed at several levels. The figure presented in a project proposal or market comparison is often the gross return, and this metric serves a useful purpose, provided that investors understand exactly what it measures and what it excludes.

Understanding the difference between gross return, net return and IRR is one of the most valuable exercises any investor can undertake before committing capital to acquisition, refurbishment and resale transactions. This is not because one figure is inherently better than another, but because each metric answers a different question and is most useful at a different stage of the analysis.

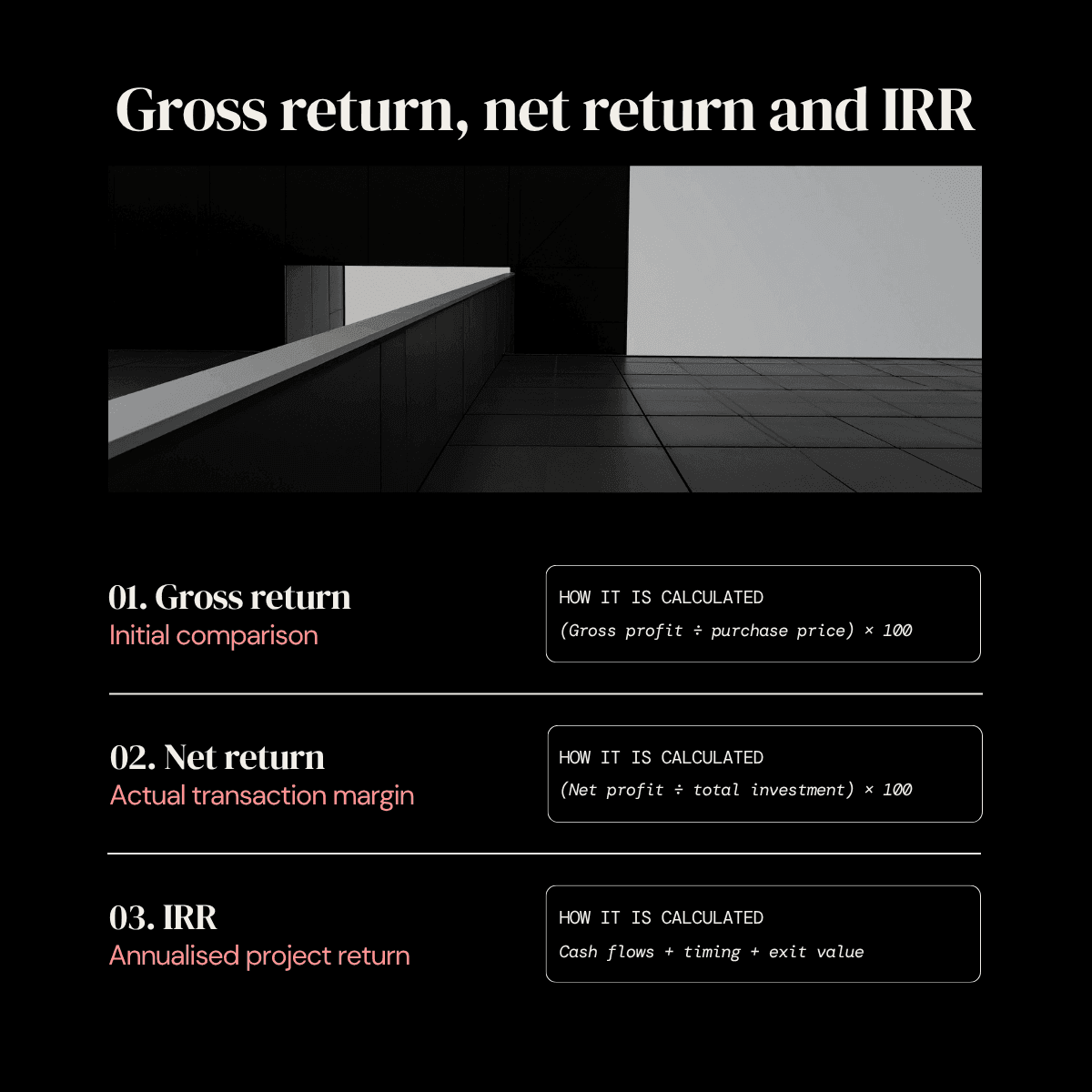

What is the gross return on a real estate transaction?

The gross real estate return measures the profit generated by a transaction in relation to the asset’s purchase price, without deducting the associated costs. It is the most straightforward formula and is commonly used as an initial indicator of attractiveness:

Gross return = (gross profit / purchase price) × 100

In an acquisition, refurbishment and resale transaction, if an asset is purchased for €150,000 and sold for €210,000 after refurbishment, the gross profit is €60,000 and the gross real estate return is 40%.

Its main purpose is to enable a quick comparison between transactions or assets. To determine whether a specific transaction is genuinely profitable, all actual costs and the time required must also be taken into account.

What is the net return and which costs does it include?

The net real estate return deducts all actual transaction costs from the gross profit before calculating the percentage return on the investment. This metric makes it possible to estimate the project’s actual performance before applying each investor’s personal tax position.

In an acquisition, refurbishment and resale transaction, the costs usually included in this calculation are:

- Acquisition taxes (property transfer tax or VAT + stamp duty), notary fees and Land Registry fees.

- Total refurbishment costs: project design, licences, construction works and contingencies.

- Financing costs where bank financing is used.

- Marketing and sale costs.

- Project management and overhead costs.

Following the previous example, a transaction generating a gross profit of €60,000 may incur between €25,000 and €35,000 in actual costs. The net real estate return would therefore be approximately 17%–23% of the purchase price. Once this figure has been calculated, each investor must apply their individual tax position to determine their final return.

Gross and net returns are therefore complementary tools: the former enables transactions to be compared quickly, while the latter assesses the actual performance of a specific real estate investment before personal taxation. According to the Bank of Spain’s Financial Stability Report, the operating margins of real estate transactions vary significantly depending on the asset type, location and strategy applied, reinforcing the need to analyse each project individually.

Why timing changes everything: the importance of IRR

Gross and net returns measure the total profit generated by a transaction, but they do not take time into account. Two real estate projects with the same net return are not equivalent if one is completed in 9 months and the other in 24 months.

To compare transactions with different timeframes, the appropriate metric is the real estate IRR (Internal Rate of Return). IRR annualises the return by taking into account the exact timing of each cash flow: the initial investment, intermediate costs and the capital recovered upon sale. Like ROI and gross return, IRR is calculated before applying each investor’s personal tax position.

For example, a transaction generating a net return of 20% over 10 months has a significantly higher real estate IRR than another transaction generating the same net return over 30 months, even though the two may appear identical on paper. The length of time for which capital remains committed represents a real cost that only IRR captures accurately.

For this reason, IRR is the most relevant metric for comparing acquisition, refurbishment and resale real estate projects: it incorporates both the return and the timeframe into a single annualised figure. You can see how this analysis is applied in our article on how to analyse a value-add real estate project.

How to calculate real estate returns in an acquisition and resale transaction

A basic process for calculating real estate returns in an acquisition, refurbishment and resale transaction involves the following steps:

1. Total purchase cost: acquisition price plus taxes, notary fees and Land Registry fees.

2. Total refurbishment cost: project design, licences, construction works and a contingency allowance of 10%–15%. To understand what should be reviewed before committing this budget, you can read our article on how to assess a property for real estate repositioning.

3. Financing and management costs: interest, overheads and marketing costs through to the sale.

4. Estimated sale price: based on actual market comparables under a conservative scenario.

5. Gross and net returns: to understand the transaction margin before personal taxation.

6. IRR: incorporating the actual schedule of capital outflows and the expected timeframe through to the sale.

7. Tax impact: applied at the end according to each investor’s individual circumstances.

This order is important because combining operating costs and personal taxation within the same calculation makes it more difficult to compare projects consistently. You can explore this approach in greater detail in our article on the key financial criteria for assessing real estate opportunities.

How these metrics are presented in structured projects

One of the advantages of accessing real estate investment through a private investors’ club is that the analytical work has already been completed before the investor makes a decision.

At balize, every project presented to the club includes a complete cost breakdown, the transaction’s ROI and the projected annual IRR. These metrics make it possible to compare real estate projects using consistent criteria. As with any type of investment, taxation is a subsequent step that each investor must apply according to their personal circumstances and country of tax residence.

Investors can participate in previously analysed acquisition, refurbishment and resale transactions from €10,000, without managing the asset directly and with an exit strategy defined from the outset.

Frequently asked questions about returns on real estate investment

What is the difference between gross return and net return in a property acquisition and resale transaction?

The gross real estate return divides the profit generated upon sale by the purchase price, without deducting any costs. The net real estate return deducts all actual transaction costs — acquisition taxes, refurbishment works, financing, management and marketing — to reflect the project’s actual margin before personal taxation. In acquisition, refurbishment and resale transactions, the difference between the two may range from 15 to 25 percentage points depending on the scope of the refurbishment and the financing costs.

Why is IRR important in property acquisition and resale projects?

The real estate IRR is the most comprehensive metric for assessing this type of transaction because it incorporates time. A transaction generating a net return of 20% over 10 months produces a significantly higher annualised return than another generating the same percentage over 30 months. IRR makes it possible to compare real estate projects with different timeframes on a consistent basis, which neither gross nor net return can achieve on their own. Like ROI, it is calculated before applying the investor’s personal tax position.

Which costs should be included when calculating the net return on a real estate refurbishment?

To calculate the net real estate return on an acquisition, refurbishment and resale transaction, the following costs should be included: acquisition taxes (property transfer tax or VAT + stamp duty), notary and Land Registry fees, the total refurbishment cost with a contingency allowance of 10%–15%, financing costs where applicable, and project management and marketing costs through to the sale. Omitting any of these items will overstate the transaction’s actual margin and lead to decisions based on an optimistic scenario that is unlikely to materialise exactly as forecast.